With regulations coming, some say DeFi will lose its edge.

They’re wrong.

“No regulation” is not the winning feature of DeFi. Neither is decentralization. Take those away and DeFi is still 100x better than TradFi.

Here’s a look at DeFi’s true competitive advantages 👇

First off, why can DeFi offer higher yields than banks?

Obviously some yields are more sustainable than others. I wrote an article a while ago looking at different types of yields.

But the reality is in the short term, the #1 reason of high yields is lots of money flowing into crypto to chase returns.

Bull & bear cycles aside, it’ll take at least a few more years for crypto to catch up w/ tradFi asset classes & for this trend to slow down.

Total global stock market cap is $120 trillion, real estate value $350 trillion. Total crypto market cap is $2 trillion. If crypto grows at the same pace as in the past 5 yrs for next 5-6 yrs, it will surpass global equity & real estate combined in market cap by 2027.

— Tascha (@RealNatashaChe) October 1, 2021

Still, large money inflow will not last forever. Those people who call DeFi a ponzi scheme have good reasons.

But keep in mind at early stage of any disruptive change, the line btw ponzi & non-ponzi is thin. You’d have to look beyond appearance. More on this in a sec.

Every startup is a ponzi scheme.

— Tascha (@RealNatashaChe) September 21, 2021

So is every new nation, religion, or crypto asset.

A ponzi is simply using money from newer investors to pay older ones. An obligatory stage for many things that grow fast.

The only difference is how much new value is also created along w/ it.

Lack of regulation is another obvious advantage of DeFi. Aave and Compound don’t have KYC. Neither are they subject to banking regulations like liquidity, capital and reserve requirements— rules that are designed to make banks safer but limit their profitability.

Alas, regulations may be a slow bus but the bus’ll arrive some day. You can try to divine the shapes they’ll take. The result is the same— increase operating cost & lower yields.

So if money inflow won’t grow forever while regulations are up & coming, what’s left to cheer for DeFi?

A lot.

Here are three killer value props of DeFi that will uphold it as an essential pillar of new financial paradigm of the 21st century.

VALUE PROP 1. LOW OPERATING COST BY DESIGN

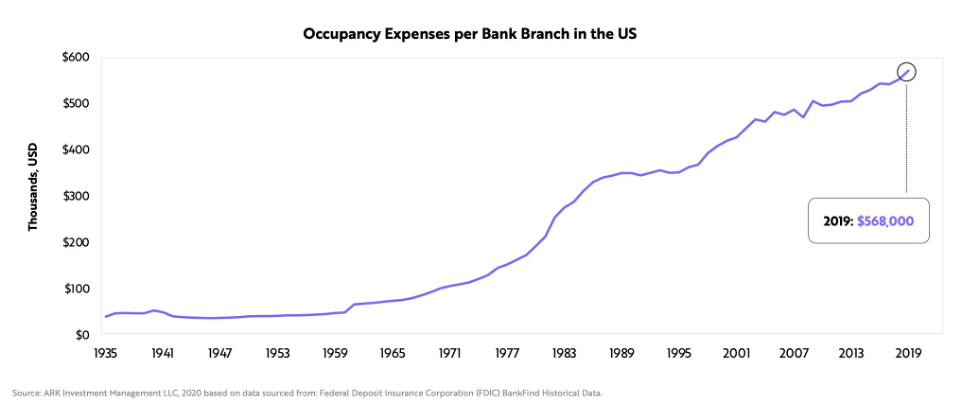

Banking is an expensive business.

A bank branch costs $600k / yr to run in the US. An average bank has 20 branches. That’s $12 million a year. And don’t forget the costs of back office, databases, security, compliance, payment network…

That’s why banking is a monopoly business hard to break into (regulations don’t make it easy either). But once you’re in, life is comfy & margins are high— the sector is the Exhibit A of resource and power concentration.

By contrast, you can spin up a DeFi app to offer deposit/lending services, i.e. “banking”, for $50-100k. Entry barrier is dramatically lower.

How did the magic happen?

The public blockchain rails that DeFi runs on—ethereum, solana, whatever— covers most of backend infrastructure cost and simplifies things a ton.

What AWS provided for millions of SaaS (software as a service) companies, blockchain is providing for DeFi. And the DeFi builders don’t need to pay for it cuz their users do and get rewarded for it (more on this in a moment).

The result is innovation and competition on steroid, at a scale unseen in the history of finance.

VALUE PROP 2: HIGH CAPITAL EFFICIENCY

As a bank you’re limited by the geographical size of your market b/c your fixed cost is high.

Say, your fixed cost is $100 and you make $10 on each loan you give. You’ll have to give 10 loans to break even. That means if a market doesn’t have the demand for 10 loans, no bank will even exist there.

That’s why in smaller countries the cost of capital is high— since the number of loans banks can make is small, banks have to earn a larger spread btw lending & saving rates to keep afloat.

And when it’s only feasible to have a small number of banks, they become monopoly powers that capture most of industry value added—> no competition—> no incentive to innovate—> cost of capital kept high—> vicious cycle continues.

By contrast, a DeFi app has one set of fixed cost with global scope of capital allocation.

If economic growth & return on capital are higher in Vietnam than in the UK, capital can be allocated from UK to Vietnam instantly. Both your British lender and your Vietnamese borrower are happier.

Meanwhile, moats are much harder to build in DeFi compared to banks since entry cost is low. All roads lead to higher efficiency and more competition that drives everyone to innovate.

VALUE PROP 3: CO-OP OWNERSHIP MODEL

The DeFi business model is participatory with investors = customers.

The customers of DeFi are also validators & stakers of the blockchains DeFi runs on. As customer, you pay for the infrastructure and reap its reward. And if you stake a DeFi platform token to provide liquidity, you get a share of DeFi profit too.

It gives customers the incentive to keep using the platform since they’re also the owners. The result is much sticker user adoption compared to TradFi.

You say, how is this different from buying the stocks of a bank you use?

Bank profit is not transparent and banks can do as they please w/ it. In reality much of it goes to executive compensation, not dividends to you.

By contrast the staking rewards of a DeFi app is programmed & trackable. If Aave lowers its staking yield, you can switch to a competitor in a blink of eyes. It creates an anti-fragile customer base w/ aligned incentives that makes the industry robust as a whole.

How about the common criticisms of DeFi that it’s not actually decentralized and is only good for speculation? Let’s talk about them.

(BTW, like this so far? I write about ideas on investment, macro and human potential. Subscribe to my newsletter for updates.)

Criticism 1: DeFi is not decentralized

None of DeFi’s long-term competitive edges require decentralization to exist.

Let’s say tomorrow JP Morgan raises some equity on NYSE and uses the money to buy up AAVE tokens and stake them (AAVE market cap is only $4 billion. If JP Morgan wants to be an AAVE whale, it’s not hard).

Since part of AAVE profits go to staking rewards, JP Morgan says, “Guys we’re keeping everything the same. The staking yields we earn, we’ll pay JP Morgan shareholders as dividends.”

AAVE still offers the same attractive rates to lenders & borrowers. It’s still 100x more competitive than any tradFi banks. Nothing has changed for users, except the decentralization maxis would be angry.

You say, but that means JP Morgan could monopolize DeFi just like in banking.

Not quite.

Since DeFi entry barrier is so low, users’ll always have plenty of other options. If you’re not happy w/ the service of AAVE, a subsidiary of JP Morgan, you’ll move your funds to Compound, Anchor, Cream… (Low entry cost of DeFi leads to intense competition, remember?)

Criticism 2: DeFi has no real use case except speculation

Financial intermediation is supposed to “intermediate”— channel the savings of an economy towards productive investments.

Critics say DeFi is doing zero of that and they are right. But DeFi is a three year old industry. What do you expect?

The various elements of a parallel financial system are being built out in DeFi as we speak, from basic saving accounts to sophisticated trading tools. Give it a minute.

A major bottleneck for DeFi to do borrowing/lending for “real world” purposes is how to use non-crypto assets— e.g. real estate, account receivables, paychecks— as collaterals.

To me the first step is to digitize those off-chain assets. All physical properties commonly used as collaterals, like houses & cars, need on-chain representation as NFTs.

There’ll be a big industry whose sole function is maintaining the linkage btw real world properties & their NFTs. Once you transfer the asset function of off-chain entities into NFTs, DeFi can take it from there.

This is not a trivial problem. (For my diamond NFT, I destroyed the underlining diamond to solve the 1-to-1 matching issue. But that’s obviously not a solution for most use cases.)

That’s why development in NFT space is so important— it’s where most collaterals in DeFi will come from to back real-world lending. Thankfully many talented folks are working on that.

Once the collateral issue is sufficiently resolved, it’ll open the flood gate of real world use cases of DeFi.

2 Comments

Ngl, I stumbled upon your bullish-on-China thread on Twitter 2 hours ago and have since read a few other posts of yours. I can already tell you’re one of the most worthwhile thinkers I’ve ever come across. So stoke to keep listening to your ideas laid out with eloquence, measure, and succinctness

To me the first step is to digitize those off-chain assets. There’ll be a big industry whose sole function is maintaining the linkage btw real world properties & their NFTs. Its here in a company called Invaniam.io